Mitchell Brandtman is excited to announce that we will once again be sharing our knowledge with you and your team through our Financier Education Workshops.

After successfully launching our Financiers’ Education Program in 2018, we are excited to be offering this program again in 2026.

This workshop has been created for Financiers who are ready to gain a more in-depth understanding of what a Quantity Surveyor does and how we help Financiers, Brokers and their clients on projects. Tass Assarapin, Partner, will be sharing his knowledge and experiences on recent NSW projects and provide valuable information on what to know in order to give you, your clients and your business an advantage on how to navigate projects in 2026.

The workshops will be held at: Level 2, 31 Market Street, Sydney 2000

This half day workshop will cover topics such as:

Role of the Financiers’ QS

Financiers’ QS Reports – Pre-funding and Progress Reports

Contracts and Procurement

Construction Costings

Construction Updates

Signs of Distressed Projects

Click on the workshop dates below to register (please ensure you list your attendance date in order of preference):

Cost to attend the workshop is $75 (ex GST) per person.

Please feel free to share this invitation with your colleagues should it be of benefit to them.

Numbers are strictly limited so register your interest now to avoid missing out.

The Mitchell Brandtman Financiers’ QS team.

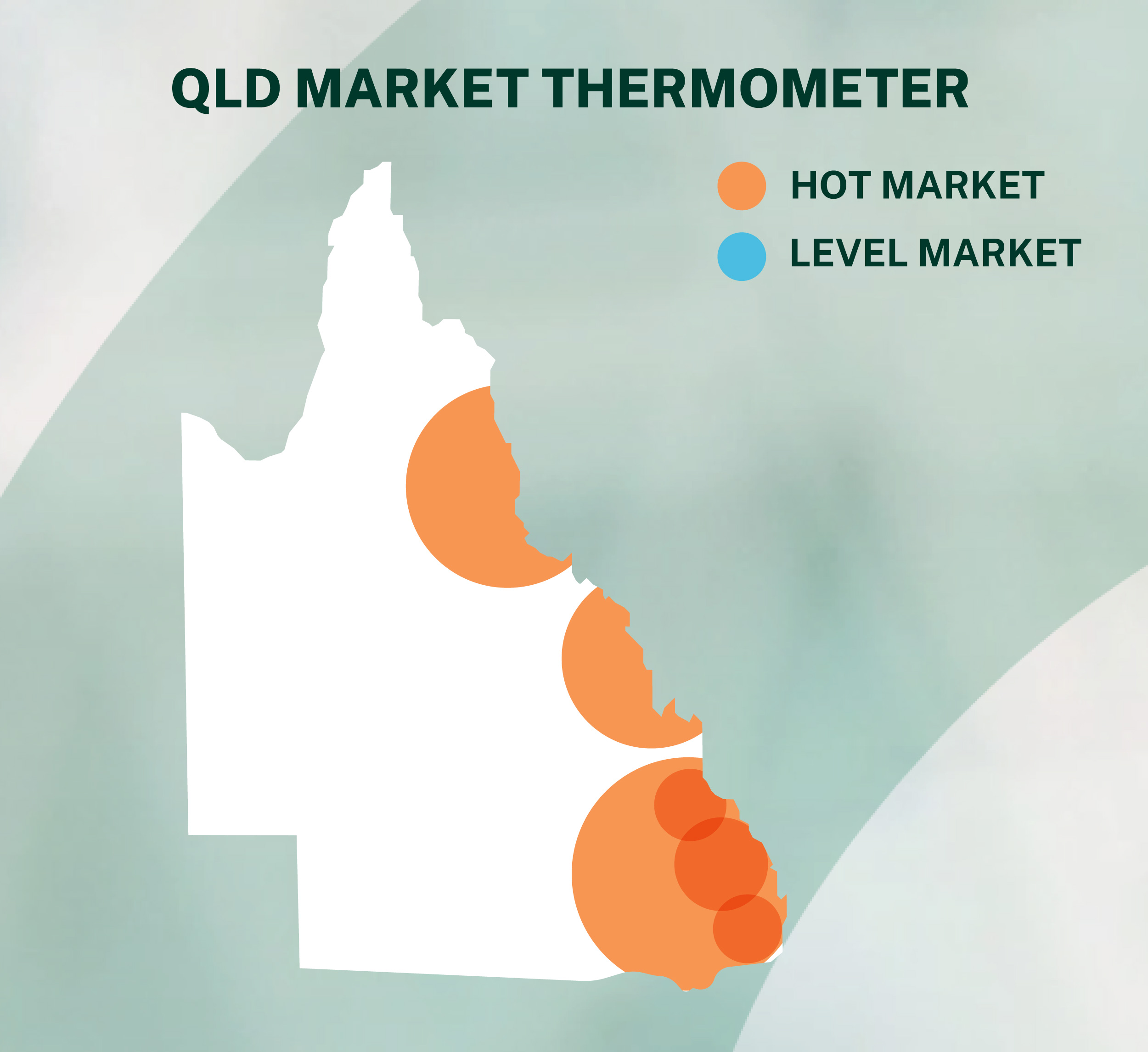

Across Australia, the construction industry is responding to new market pressures and changing buyer behaviour, and Canberra is no exception. The region is steady, quieter than surrounding cities, but still moving through an important transition. Residential demand has shifted, commercial arenas are weaker than they have been in years, and developers are reconsidering where the real long-term value sits. In the middle of these changes, Quantity Surveyors are becoming increasingly important to forecast certainty from planning to completion.

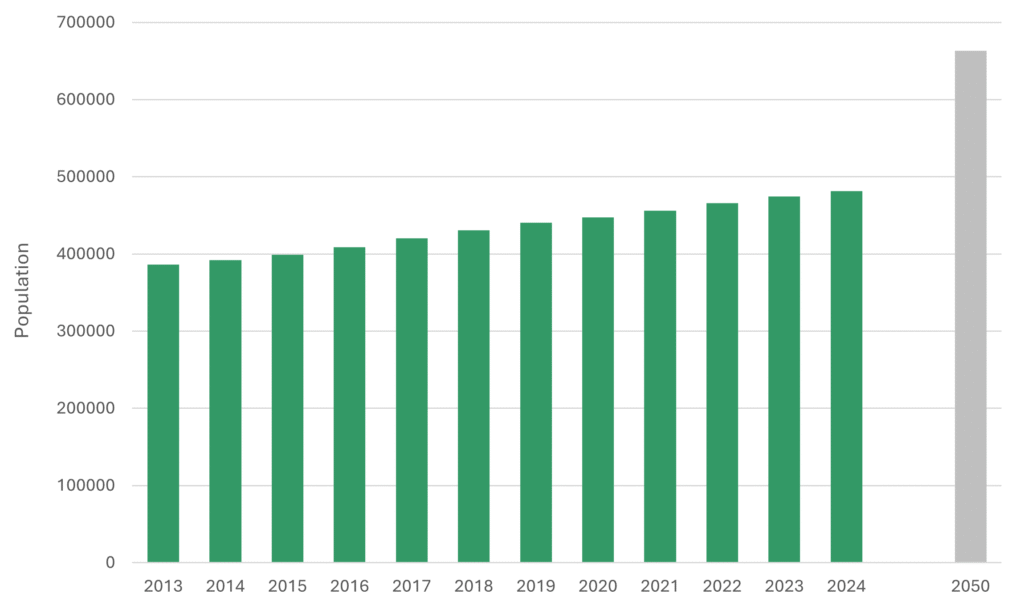

Canberra’s population data provides helpful context for how development has been tracking. At the end of December 2024, ACT reached an estimated 481,677 residents. This was a quarterly rise of about 0.3 percent and a yearly growth of 1.4 percent, which is slightly slower than the national rate of 1.7 percent. Over the past decade, the ACT has added more than 70,000 people with an average increase of around 7,000 each year.

Source: ABS

Recent growth has been shaped mostly by natural increase and overseas migration, while interstate migration has been negative, with more residents leaving than arriving. These patterns influence who developers are building for, how quickly projects move and what types of dwellings find buyers.

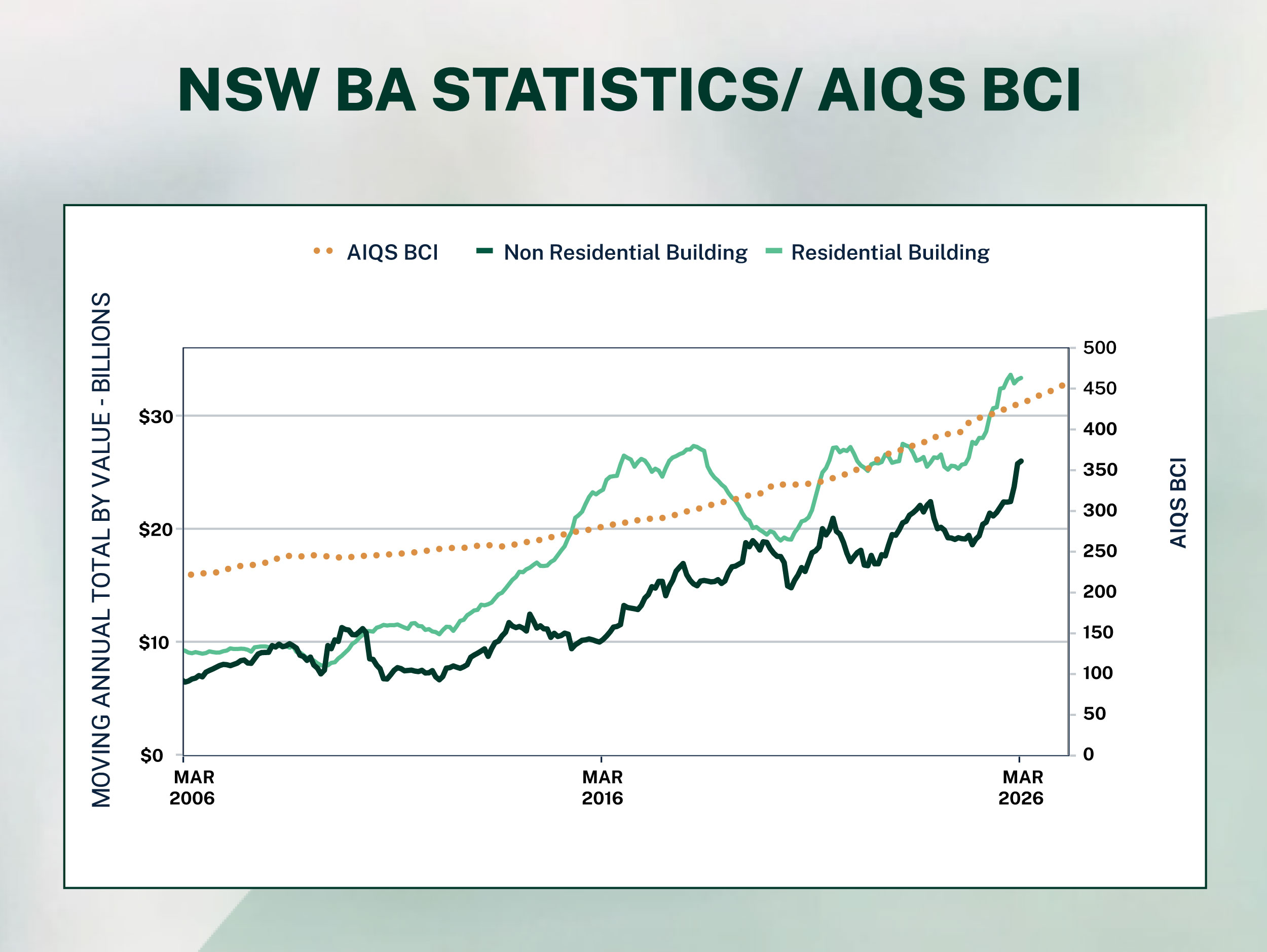

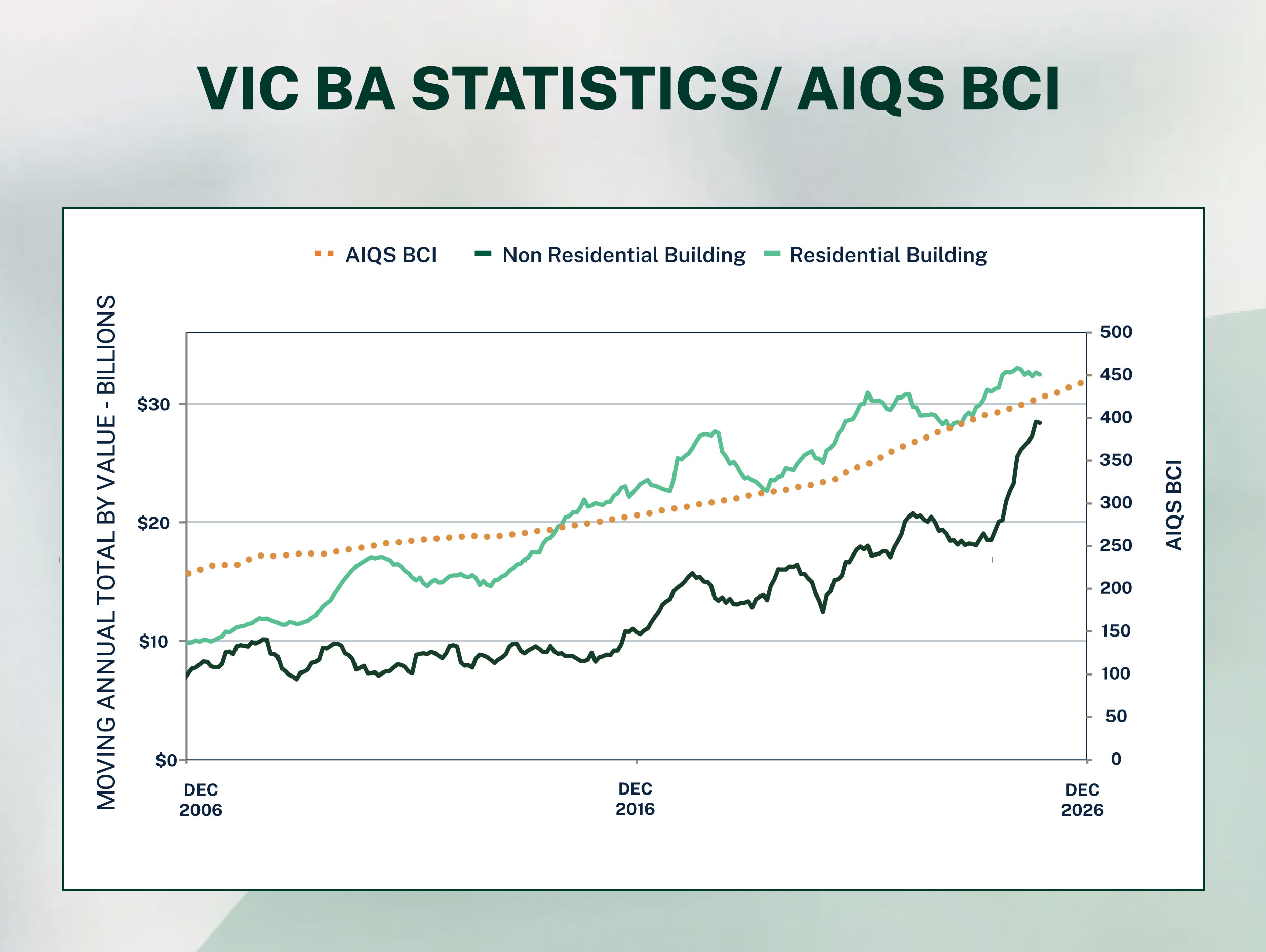

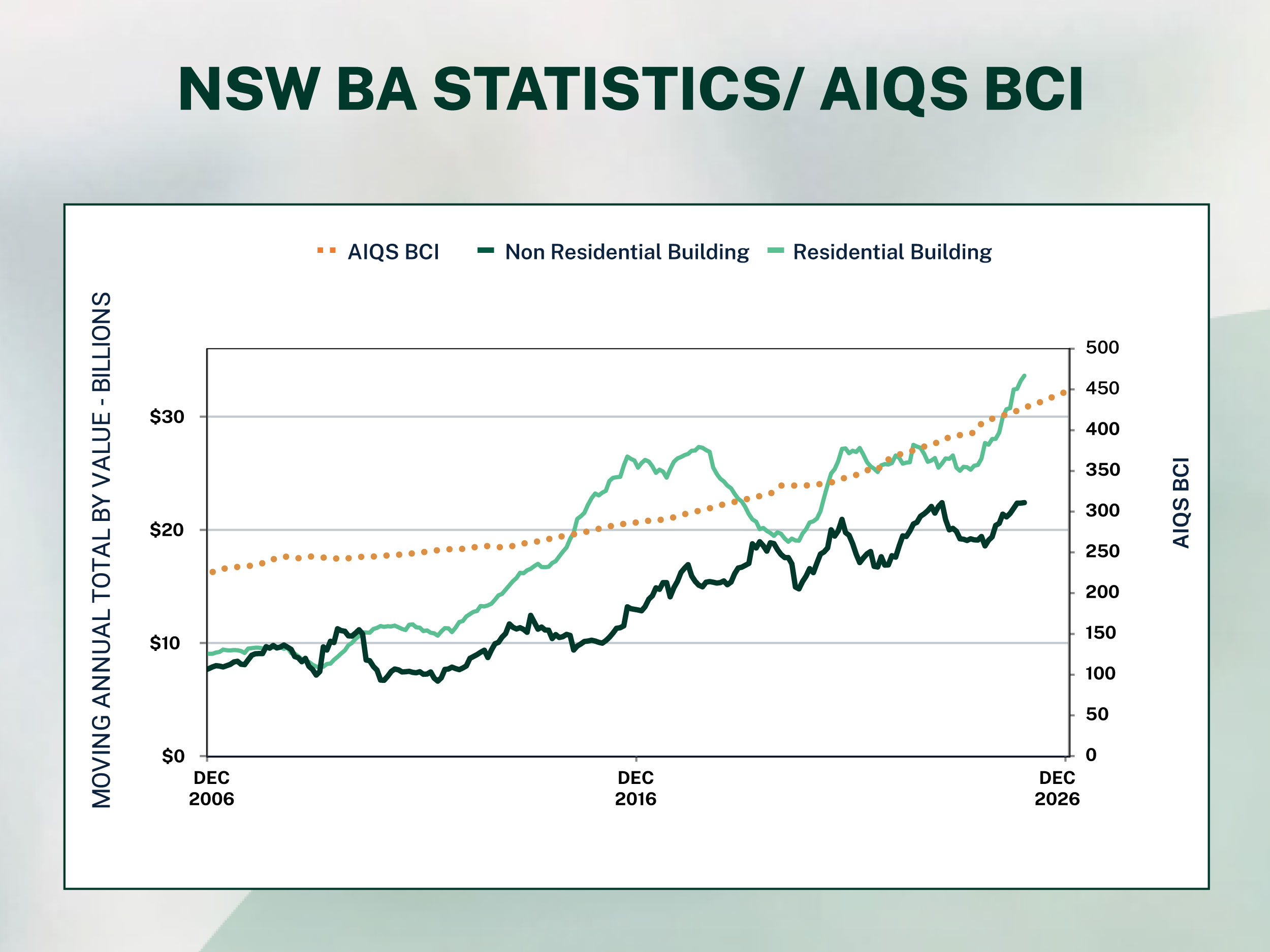

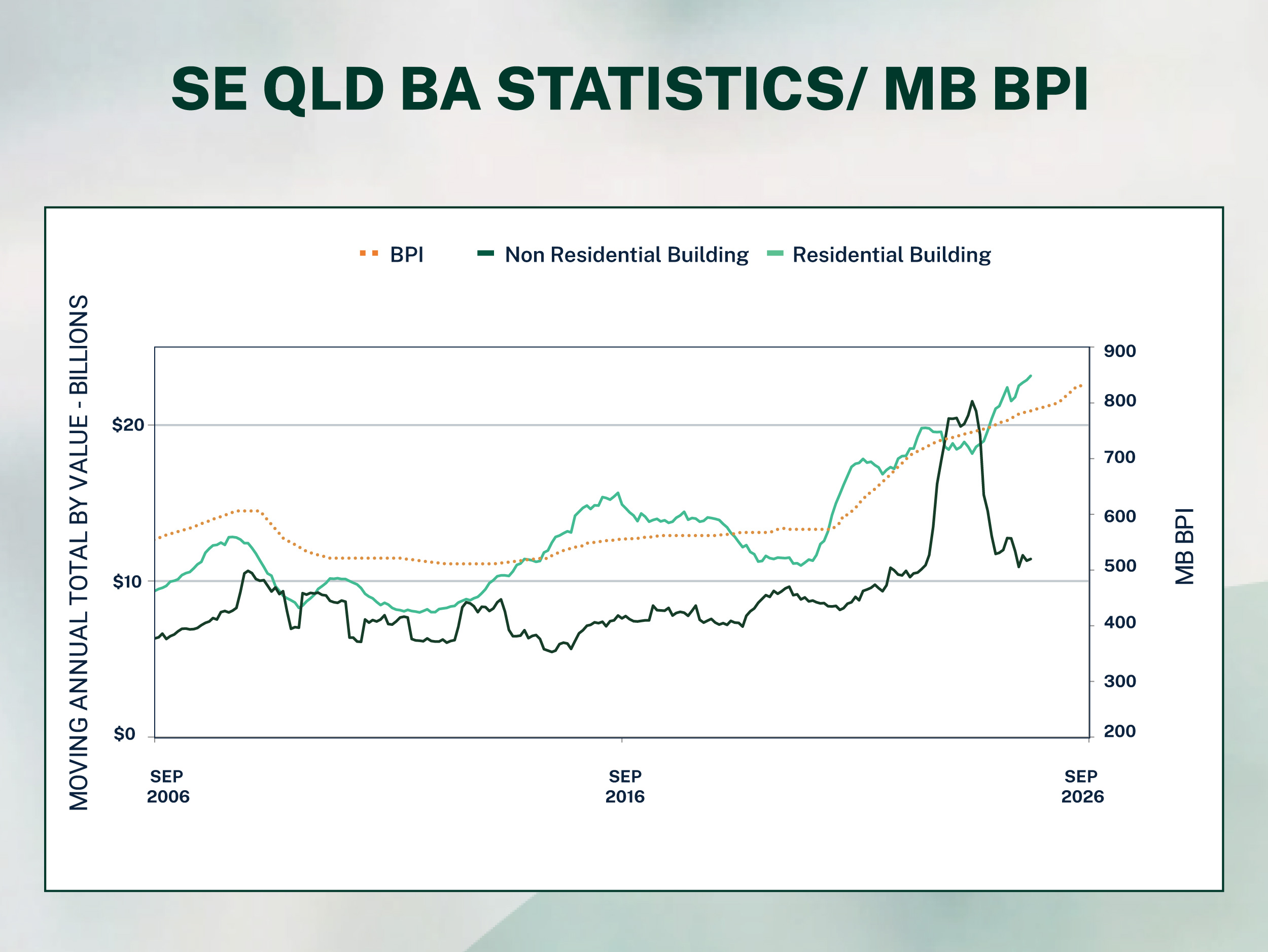

Residential approvals highlight this shift. In the 2024 to 2025 financial year, the ACT recorded only about 2,731 new dwellings approved, well below the annual target of 4,212 needed to meet the territory’s contribution to the National Housing Accord (Source: Property Council of Australia). Industry groups have described it as the slowest year for approvals in nearly twenty years. Monthly data has been mixed. In May 2025, the number of dwellings approved in terms of ‘trend’ fell 8 percent compared with the previous year. Yet April 2025 showed an 8.6 percent increase in approvals when compared month to month. By June 2025, approvals lifted further, reaching about 695 new dwellings, almost double the monthly target suggested under the Accord. The value of construction work done in the June quarter of 2025 increased by 17.5 percent in the ACT, although national data shows that this lift came mostly from non-residential projects.

Source: ABS

A moving annual total is the sum of the last 12 months of data at any point in time, providing a smoothed view of the underlying trend.

These figures reflect a market that is still active but moving unpredictably. According to Mitchell Brandtman’s Canberra Partner, Shane Brandtman, commercial buildings are a challenge with high vacancy levels, while residential sentiment varies between suburbs. Build-to-rent has become one of the more promising paths for developers, not only in central areas but also in locations around the ACT such as Murrumbateman, Sutton, Googong and Yass. These edges of Canberra are attracting strong rental demand and continue to provide a more workable model, partly because returns are based on the total cost of construction rather than the slower sales experienced in the current apartment market.

Developers who we work with describe Canberra’s rental market as consistently strong. Construction prices remain lower than in many other cities, which helps build-to-rent developers who benefit when total project costs are controlled. In his view, the long-game nature of build-to-rent is what makes it attractive. The value is in holding stock until improved conditions lift returns across the portfolio.

However, apartment sales paint a different picture. Some pockets, particularly in the inner north and inner south, continue to perform because they appeal to owner occupiers and downsizers. But other projects have not reached expectations. With construction costs above what the market could support, these projects struggle and are expected to remain slow for some time.

These challenges have led developers to rethink their strategies. Many are using this period to progress development approvals, refine designs and prepare sites for the next cycle rather than pushing large new projects to market immediately. Several are also looking outward to land subdivisions, industrial sites and rural residential opportunities near the ACT. Some are focusing only on build-to-rent within Canberra until the market catches up to the returns needed to justify larger projects.

Subcontractors & Skilled Labour

One consistent message from developers is the growing pressure on subcontractors and skilled labour. The workforce continues to move north toward Queensland due to the strong pipeline and the upcoming Olympics. This shift has raised concerns about future pricing. If Canberra’s market becomes more active, the limited number of subcontractors may lead to higher quoting levels as trades prioritise jobs with stronger margins. Some subcontractors are currently accepting lower returns just to maintain workflow for their teams. The question is how long they can sustain that approach.

This is where Quantity Surveyors become essential. With constant changes to labour rates, material prices and subcontractor capacity, developers need accurate figures early and often. Some developers we have consulted for noted that many firms have been caught out in recent years by relying on assumed prices rather than current numbers. This highlights that the relationship between a developer and a Quantity Surveyor is most valuable when it produces real time cost understanding during feasibility. Better clarity at that stage influences funding decisions, design choices and ultimately the success of the project.

At Mitchell Brandtman, this approach mirrors how our teams work across the construction project lifecycle. Quantity Surveyors gather and interpret information from a range of sources, track local movements in pricing and use that to guide project direction before the first contract is signed. As Canberra’s cost environment continues to shift, the ability to update estimates quickly, identify where risk sits and support funding submissions becomes central to project certainty. It also supports a smoother construction stage because the builder and developer both begin the project with shared expectations.

Government policy is another factor shaping the environment. Post-covid, many are choosing to pursue work in other States. Even so, government projects within Canberra continue to contribute strongly to the overall construction workload. These projects also influence wages and subcontractor availability, which flows through to private sector work. While the settings may feel challenging now, the presence of strong public projects will help maintain skilled labour in the region, which will be important when the private market strengthens again.

Looking Ahead

Looking ahead, developers expect the most successful projects in the next five to ten years to be smaller in scale and more targeted to owner occupiers. Projects between about 30 and 100 units in the inner suburbs are likely to perform better than larger schemes in outer areas. Build to rent will continue to be promising if developers can control costs below prevailing market rates and secure well priced land. Buyers and tenants in Canberra are not yet willing to pay for premium sustainability features in residential buildings, so keeping the operational costs low will remain a priority.

Canberra may be quieter than other cities today, but it is still preparing for another period of growth. The region remains stable, the rental market is strong, and the surrounding areas are attracting increasing interest. Projects that succeed will be those built on good market insight, realistic cost planning and early collaboration between developers, designers, subcontractors and Quantity Surveyors. With the right groundwork, the next cycle in Canberra has the potential to offer solid opportunities for those who understand what is to come and invest with a long view.

This Mitchell Brandtman Quarterly Construction Cost Update

has been put together to help keep you informed on the

movements of the market to better position yourself for your